How to Read an Explanation of Benefits (EOB) from a Health Insurance Carrier

Health insurance carriers are required to provide EOBs for all medical claims – showing the breakdown of charges, how the plan paid for the care received, and how much of the charge(s) are being passed on to the Member.

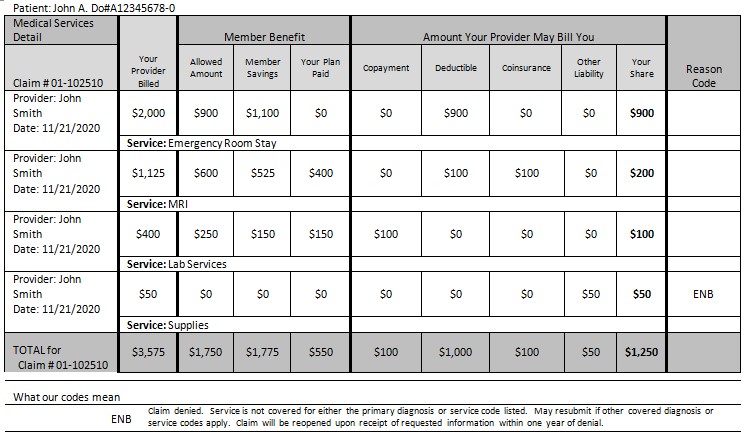

Below is a sample EOB for a member that has a $1,000 Deductible, 80/20 coinsurance, $100 lab copay and has not satisfied any of their deductible or max-out-of-pocket (MOOP).

· Column 1 – Provided Service and Date. This will show the service provided, the name of the provider, and the date of service(s).

· Column 2 – Provider Charge Amount. This amount provides the list price for each service. Remember, this is similar to the MSRP, and no one is expected to pay this amount. Often times it’s many times more than what they would accept for the service.

· Column 3 – Allowed Amount. This is the maximum that the insurance plan said it will pay for that service. Often times referred to as the “Negotiated Rate”.

· Column 4 – Member Savings. This illustrates the cost reduction to the member for having the benefit of the carrier’s negotiated rate.

· Column 5 – Your Plan Paid. This column shows the amount a member’s insurance plan paid – in the event there are applicable copays, or a member had already hit their deductible or max-out-of-pocket. Notice, in the example, the plan paid on the MRI (because coinsurance kicked in) and on the Lab services (because the member had a copay).

· Column 6 – Copayment. The copay is a fixed number that the member must always pay for that service, until they hit their MOOP. In the example above, the member had a $100 copay for lab services.

· Column 7 – Deductible. This is the amount that must be paid, out of the member’s pocket, before insurance policy benefits will apply. In the example above, the member had to pay the entire allowed amount on their ER stay, but hit the deductible after $100 of paying the MRI. At this point, the member will not have to satisfy any more of their deductible until the accumulators start over (typically based on calendar year).

· Column 8 – Coinsurance. The coinsurance is based on a percentage of the allowed amount that the member must pay, AFTER the deductible has been satisfied. Examples are 80/20, or something similar, with 80% being what the insurance plan would pay and 20% being what the member is responsible for paying, AFTER they have met their deductible. In the example above, after the member paid $100 towards the MRI, and hit their deductible, $500 in charges remained. The member is responsible for 20%, so the member had to pay $100 in coinsurance, while the plan paid the remaining $400 (80%).

· Column 9- Other Liability. This typically designated cost of services not covered or denied. Look for reason code and explanation of codes for explanation.

· Column 10 – Your Share. This is a sum total the member is responsible for under columns 6, 7, 8, & 9.

Yes, EOBs can be a bit confusing, but it cannot be stressed enough how important it is to be able to read them. Members should only pay their medical bills based on the EOB. Check to make sure the provider charges are accurate and that they were accurately run through the insurance plan. Then pay only “Your Share”. EOBs can vary in layout from one carrier to another, but the terms are standard. For specific questions about a charge or denial, reach out to your insurance company. The Customer Service/Member Services number should be on the back of your insurance card.

Back to Member Resources

|